Navigating Taxes & Compliance as a Web3 Freelancer

Understand the 7 key areas of taxation and compliance for freelancers receiving payments in crypto.

.png)

As a freelancer working for Web3 companies and DAOs, getting paid in crypto means also having to think about taxes and compliance with financial reporting rules to prevent money laundering.

Here are 7 key things to note about tax and compliance as a freelancer getting paid in crypto.

Ready to Supercharge Your Crypto Accounting?

Stop wasting time, manually creating journal entries. Automate your accounting now, and enjoy error-free reporting

Learn how to scale your company's crypto & fiat financial operations

Your financial complexities are our specialties. Schedule your free consultation today and discover how Request Finance can transform your financial operations

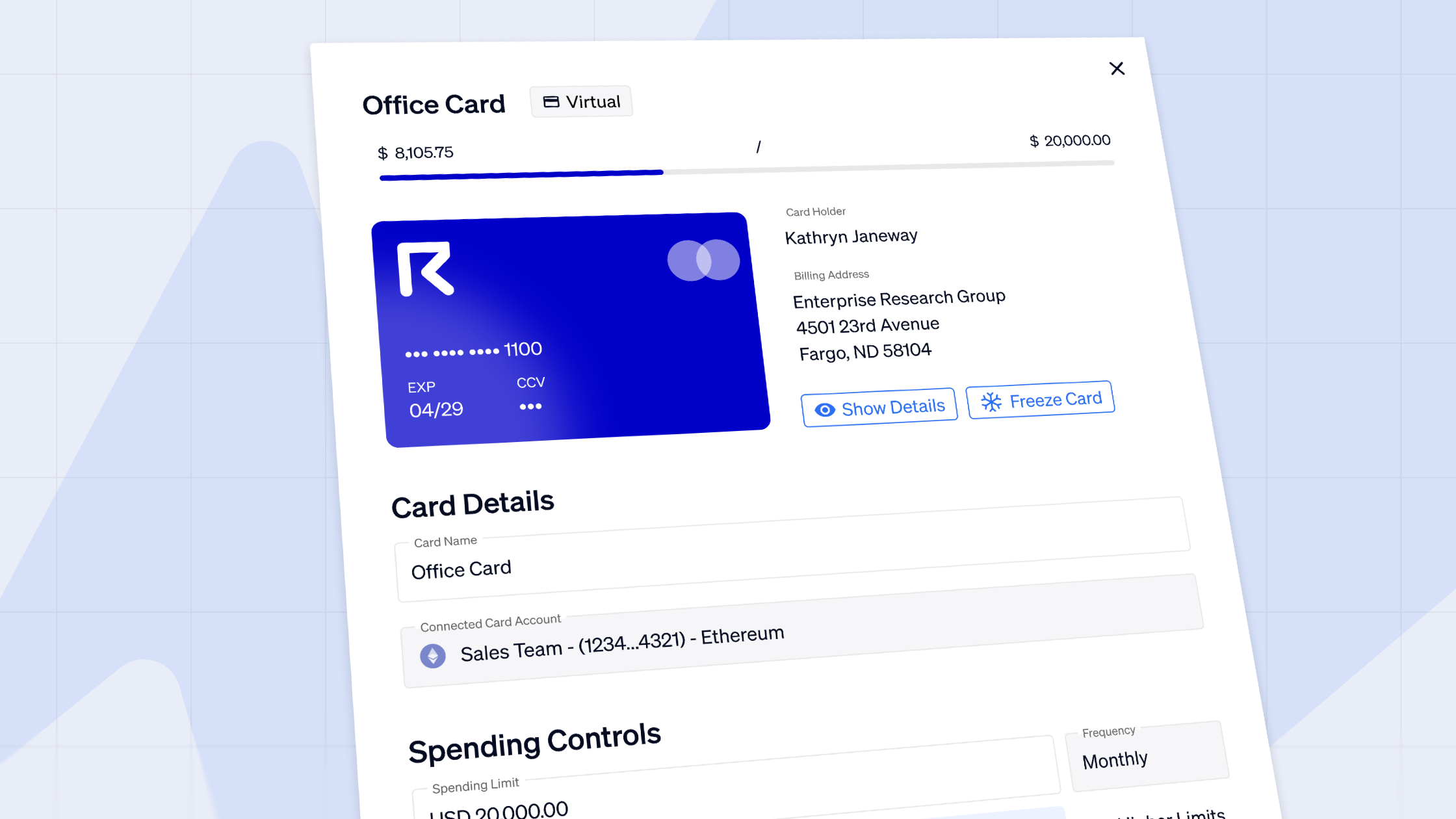

Simplify crypto and fiat financial operations today

Rely on a secure, hassle-free process to manage your crypto invoices, expenses, payroll & accounting.

1. Digital assets are taxable property

The IRS treats digital assets such as cryptocurrencies, stablecoins, and non-fungible tokens (NFTs) as property for tax purposes. This means that any income or gains from receiving, selling, exchanging, gifting, or disposing of digital assets are subject to tax. Freelancers must report all digital asset-related income on their tax return, regardless of the amount or frequency of transactions.

2. Digital asset transactions must be valued in U.S. dollars

The IRS requires that the fair market value of digital assets be determined in U.S. dollars at the time of receipt or disposition. This means that you must keep track of the exchange rate or price of the digital assets received or disposed of, and use a consistent method to calculate their value using historical exchange rates or prices for digital assets.

3. Digital asset income is subject to self-employment tax

If you receive digital assets as payment for your freelance services, you must include the fair market value of the digital assets in their gross income. This income is subject to self-employment tax, which is 15.3% of the net earnings from self-employment.

4. Digital asset gains and losses are subject to capital gains tax

If you sell, exchange, gift, or otherwise dispose of digital assets, you must report any gains or losses on their tax return. The amount of gain or loss is the difference between the fair market value of the digital assets at the time of disposition and their adjusted basis, which is usually their cost.

The gain or loss is classified as short-term or long-term depending on how long you held the digital assets before disposing of them. Short-term gains and losses are taxed at ordinary income tax rates, while long-term gains and losses are taxed at preferential capital gains tax rates.

5. Digital asset rewards and awards are taxable income

If you receive digital assets as a reward or award for participating in Web3 and crypto activities, such as mining, staking, airdrops, forks, or bounties, you must include the fair market value of the digital assets in their gross income.

This income is also subject to self-employment tax if it is related to your trade or business as a freelancer.

You may be able to deduct some of the expenses associated with these activities, such as electricity and equipment costs.

6. Digital asset donations are deductible expenses

If you donate digital assets to a qualified charitable organization, you may be able to deduct the fair market value of the digital assets as a charitable contribution on their tax return. However, you must have held the digital assets for more than one year to claim the deduction at fair market value; otherwise, you can only deduct their adjusted basis. You must also obtain a written acknowledgment from the charity for any donation of $250 or more.

7. Digital asset transactions must be reported

Beyond tax purposes, financial authorities often require that digital asset transactions are reported for anti-money laundering purposes. In the U.S., freelancers must fill in certain forms to the IRS.

Digital asset transactions must be reported on Form 1099. If you receive or pay more than $600 worth of digital assets in a calendar year from any single payer or payee, you must report these transactions on Form 1099. The payer or payee must also receive a copy of Form 1099 by January 31 of the following year. You can use a crypto tax software service such as TaxBit to generate and file Form 1099 electronically.

Digital asset transactions must be answered on Form 1040. The IRS has added a question at the top of Form 1040 that asks whether you received, sold, exchanged, gifted, or disposed of any digital assets during the tax year. Failure to answer this question correctly could result in penalties or audits by the IRS.

As you venture into Web3 freelancing, remember that compliance is key.

Arm yourself with the right knowledge, utilize the right tools, and you can make the most of your Web3 freelance career while confidently adhering to all necessary regulations.

Crypto finance tips straight to your inbox

We'll email you once a week with quality resources to help you manage crypto and fiat operations

Trending articles

Get up to date with the most read publications of the month.

Our latest articles

News, guides, tips and more content to help you handle your crypto finances.

Master your crypto spend management now

Take control of your crypto spend management while relying on our safe and secure process.