What Web3 CFOs can Learn from Silicon Valley Bank’s Collapse

In this article, we highlight actionable insights on what lessons crypto companies, DAOs, and DeFi protocols can learn from the fastest bank run in history.

There has been much ink spilled already on the causes, and consequences of Silicon Valley Bank’s collapse. In this article, we highlight actionable insights on what lessons crypto companies, DAOs, and DeFi protocols can learn from the fastest bank run in history.

Here are some risks Web3 CFOs, and DAO treasury managers should watch out for.

Ready to Supercharge Your Crypto Accounting?

Stop wasting time, manually creating journal entries. Automate your accounting now, and enjoy error-free reporting

Learn how to scale your company's crypto & fiat financial operations

Your financial complexities are our specialties. Schedule your free consultation today and discover how Request Finance can transform your financial operations

Simplify crypto and fiat financial operations today

Rely on a secure, hassle-free process to manage your crypto invoices, expenses, payroll & accounting.

1. Counterparty risks

Counterparty risk is the likelihood or probability that one of your borrowers, service providers - or their counterparties - might be forced to default, or knowingly violate their contractual obligations.

Centralized stablecoins like USDC and USDP are often marketed as transparent, reliable, and stable. There are good reasons to believe that. However, it is worth remembering that even in the absence of fraud, or gross negligence on the part of stablecoin issuers, things can and do go wrong.

For one, stablecoin issuers like Circle are reliant on their own counterparties like Silicon Valley Bank. Even though it was two-orders removed from USDC users, its collapse led to a transmission of that risk to stablecoin holders. This in turn, mutated into market risk, as sell pressure on USDC’s caused its price to de-peg from the USD, affecting everyone who was using USDC, or holding it on their balance sheets.

More recently, we have also witnessed counterparty risk in the form of regulatory action. When Paxos, the issuer of BUSD, was served a Wells Notice by the United States’ Securities and Exchanges Commission (SEC). Although Paxos guarantees the 1:1 redemption of BUSD for USD, the panic that ensued caused a minor, short-lived de-peg.

2. Market risks

Market risk stems from exposure to price movements. This includes things like currency exchange rates, and interest rates.

Most people are familiar with the risks of holding volatile cryptocurrencies on their balance sheets. The Chainalysis State of Web3 Report noted that the average DAO with assets over $1 million suffered a maximum drawdown of 51% over 2021, while Bitcoin saw a maximum drawdown of 72% that year.

High-quality stablecoins like USDC have thus far been considered a safe haven asset within many crypto treasuries at companies, DAOs, and crypto funds. But the events surrounding Circle’s exposure to SVB highlights that there is a need to diversify, or hedge one’s exposure to a single stablecoin, denominated in a single currency (USD). Holding a basket of stablecoins from different issuers (e.g. USDC, USDP, USDT, DAI), and different currencies (e.g. XSGD, EURe, jCHF) might help protect portfolios and treasuries from such events.

More fundamentally, SVB’s collapse highlights that crypto asset prices can also be affected by interest rates - but not in the way most people think. It is fairly common knowledge that low interest rates drive asset prices - including in crypto - up due to the lower costs of borrowing.

However, what few realize is that the prolonged low interest rate environment we have seen over the past decade has created business models, and entire segments of the economy dependent on cheap and abundant capital, and rising asset prices. One of those being SVB, and much of its depositor base - venture-backed tech startups.

In contrast to other banks, low interest rates meant SVB’s depositor base found it easier to raise funds, and thus actually deposit more into SVB. The reverse happens when interest rates are hiked aggressively. SVB’s depositors deposit less, and also withdraw more as they go out of business, or seek better yields elsewhere to deploy their funds.

So while Circle, and the business model of issuing stablecoins actually benefit from interest rate hikes, at least one of Circle’s counterparties, SVB, did not. And this market risk to SVB, ultimately mutated into counterparty risk for Circle, which further mutated into market risk for all holders and users of the USDC stablecoin.

3. Liquidity risks

The fall of Silicon Valley Bank, is being described as the fastest bank run in history. In an internet age, with social media and instant communications, rallies and crashes in financial markets are not only more extreme in magnitude, but also faster. The diffusion of information (reliable or not) spreads at the speed of a tweet.

Arguably, our current model of fractional reserve banking, and quarterly financial reporting has become ill-suited to our networked age. Liquidity crises can very quickly become solvency crises - all of which hangs on the confidence of depositors and investors. Confidence, as we all know, is an incredibly fragile thing in an internet age.

At the core of this fragility, is the lack of access to independently verifiable, real-time financial reports. Unlike with on-chain data, there is little way for anyone to see in real time, the financial health, or activity of an organization, or its key actors. This opacity makes it difficult for people to make up their own minds, which breeds herd behaviors in financial markets.

For instance, nobody really had any good way of knowing how exposed Circle was to Silicon Valley Bank, except for relying on their public statements. Thus, the rational thing for most people to do, was to assume the worst, and rush to make redemptions en masse, or sell off their USDC at deep discounts to the promised exchange rate, further fueling fears. At its lowest point, USDC was sold down to $0.879 (a 13% discount to peg) even though the fullest extent of Circle’s exposure to SVB was ultimately revealed to be only $3.3 billion of its $40 billion (8.25%).

It seems that we may have evolved to assume the worst, and err on the side of caution. A rustling in the grass might be a lion, or something more benign like the wind. But fewer of our optimistic ancestors lived long enough to pass on their predisposition for assuming the latter.

Actionable insights

1. Implement a risk monitoring and management system

Identify and categorize risks:

- Liquidity risks

- Market risks

- Operational risks

- Counterparty risks

Evaluate risks:

- Probability x Cost

Decide on responses to risk:

- Accept, or avoid altogether?

- If the risk is accepted, then can it be transferred/transformed, or controlled?

Report on the risk

- Evaluate effectiveness of responses

- Monitor ongoing levels of risk, and exposures to evolving risks

-

2. Take an ecosystem view of risk

As the global economy becomes more enmeshed, risks can cascade, and spread rapidly. A virus outbreak in China brought the entire global economy to a standstill. The collapse of SVB could have wiped out a major currency of the entire crypto economy.

Don’t just identify risks from your main counterparties - but theirs too. Consider not just your own borrowers, customers, investors, lenders, and service providers. Their risk exposures may turn out to be just as important as your own.

3. Take an evolutionary view of risk

Identify what sustained macro environmental conditions, or operating assumptions your industry has come to take for granted.

Then assess: (i) the possible causes of a macro “climate change”, (ii) which parts of your ecosystem might be the most vulnerable, and (iii) what mechanisms of transmission - i.e. sequence of falling dominoes - might ultimately expose you to those risks.

Concluding thoughts

“Great marketing only makes a bad product fail faster", is a quip often attributed to the British advertising tycoon, David Ogilvy. Great technologies like DeFi, or the internet, often make bad economic models fail faster.

They magnify existing vulnerabilities, whether in traditional finance, or decentralized finance. History is replete with examples of this: from the subprime mortgage crisis of 2008, the collapse of SVB in 2023, or the graveyards of 2022 littered with the empty shells of “play-to-earn” NFT games, collapsed crypto lenders, and the abortive UST stablecoin by Terra.

That does not mean that the technological advances, and new business models made possible by blockchain primitives are worthless. Quite the opposite. One of the promises of an on-chain economy is the possibility of independently verifiable, real time financial reporting. As dry as it may sound, it could help to prevent not only fraud, but also counteract crises of confidence that lead to bank runs, or the dumping of a collateralized stablecoin.

Independent verifiable financial statements serve as a Schelling point enabling people to achieve collectively rational outcomes. In game theory, a focal point (or Schelling point) is a solution that people tend to choose by default, in the absence of communication. Without it, people will just all defect, and act selfishly - resulting in collectively suboptimal outcomes.

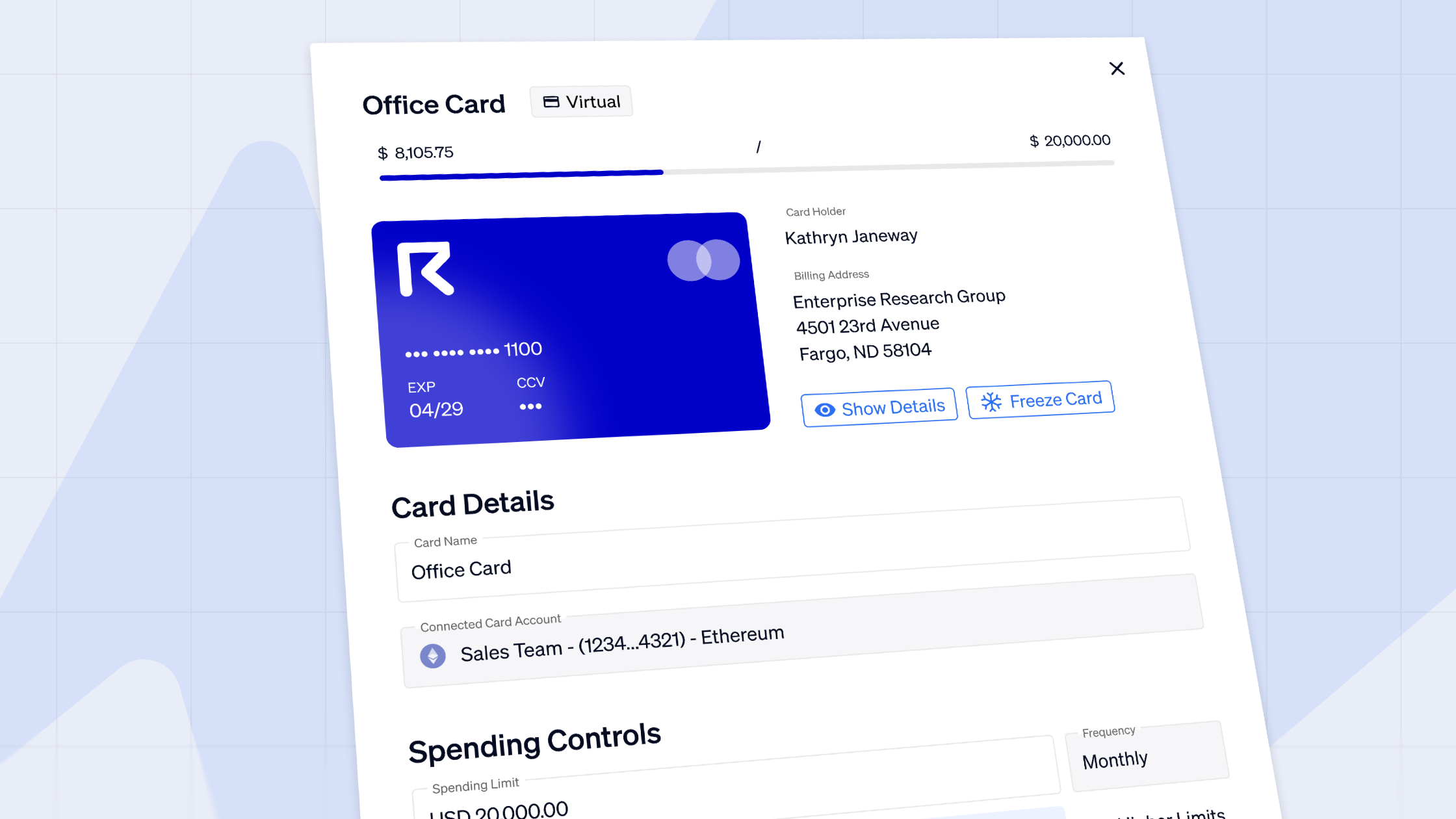

Using the right tools to manage your company or DAO's treasury management operations in crypto, can go a long way to help to provide clarity on your organization's financial health. Over 2,000 Web3 teams have used Request Finance to simplify financial reporting and payments, of nearly $290 million in crypto payroll, expenses, and invoices.

Crypto finance tips straight to your inbox

We'll email you once a week with quality resources to help you manage crypto and fiat operations

Trending articles

Get up to date with the most read publications of the month.

Our latest articles

News, guides, tips and more content to help you handle your crypto finances.

Master your crypto spend management now

Take control of your crypto spend management while relying on our safe and secure process.