Methods and Best Practices for On-Ramp and Off-Ramp in the Crypto Landscape

On-ramp vs Off-ramp: Explore best practices to navigate the complexities and risks involved in the process.

Discover more actionable insights from finance and operations professionals at leading Web3 companies, DAOs, and Foundations by downloading our Web3 CFO Guide.

In the world of DeFi and TradFi, the movement of value between crypto wallets and bank accounts is not a straightforward process. Fiat currencies on banking rails and cryptocurrencies on blockchain networks operate on separate technology stacks, making direct transfers between them impossible. To bridge this gap, the concept of on-ramps and off-ramps was introduced.

On-ramp and off-ramp, as their names suggest, are two sides of the same coin. On-ramps simply mean the exchange of fiat currencies for crypto. Off-ramps refer to the reverse: the exchange of crypto for fiat.

Methods to On Ramp and Off Ramp

There are presently four primary means to on ramp and off ramp:

1. Centralized stablecoins

2. Decentralized stablecoins

3. Centralized exchanges

4. On-ramp vs Off-ramp: service providers

1. Centralized stablecoins

Stablecoins are cryptocurrencies that are pegged to a fiat currency, such as the US dollar. Centralized stablecoins, like USDC and USDT, are issued by centralized entities who promise 1:1 exchanges between fiat currencies and stablecoins. USD-denominated stablecoins as a whole continue to be a popular choice for enterprise crypto payments, making up over half, or 54% of the crypto payments on Request Finance.

To convert fiat currency into stablecoins, you simply deposit your fiat into the issuer's bank account, and in return, they mint or issue an equivalent amount of stablecoins into your preferred crypto wallet. Once you have the stablecoins, you can use them for making payments to other crypto wallet addresses or exchange them for other types of cryptocurrencies on a cryptocurrency exchange. The process of redeeming stablecoins for fiat follows the same pattern but in reverse.

Typically, to engage with these centralized entities, you would need to apply for a business account. Some of these entities are directly integrated into crypto wallets and payment apps, making them easily accessible from within these platforms.

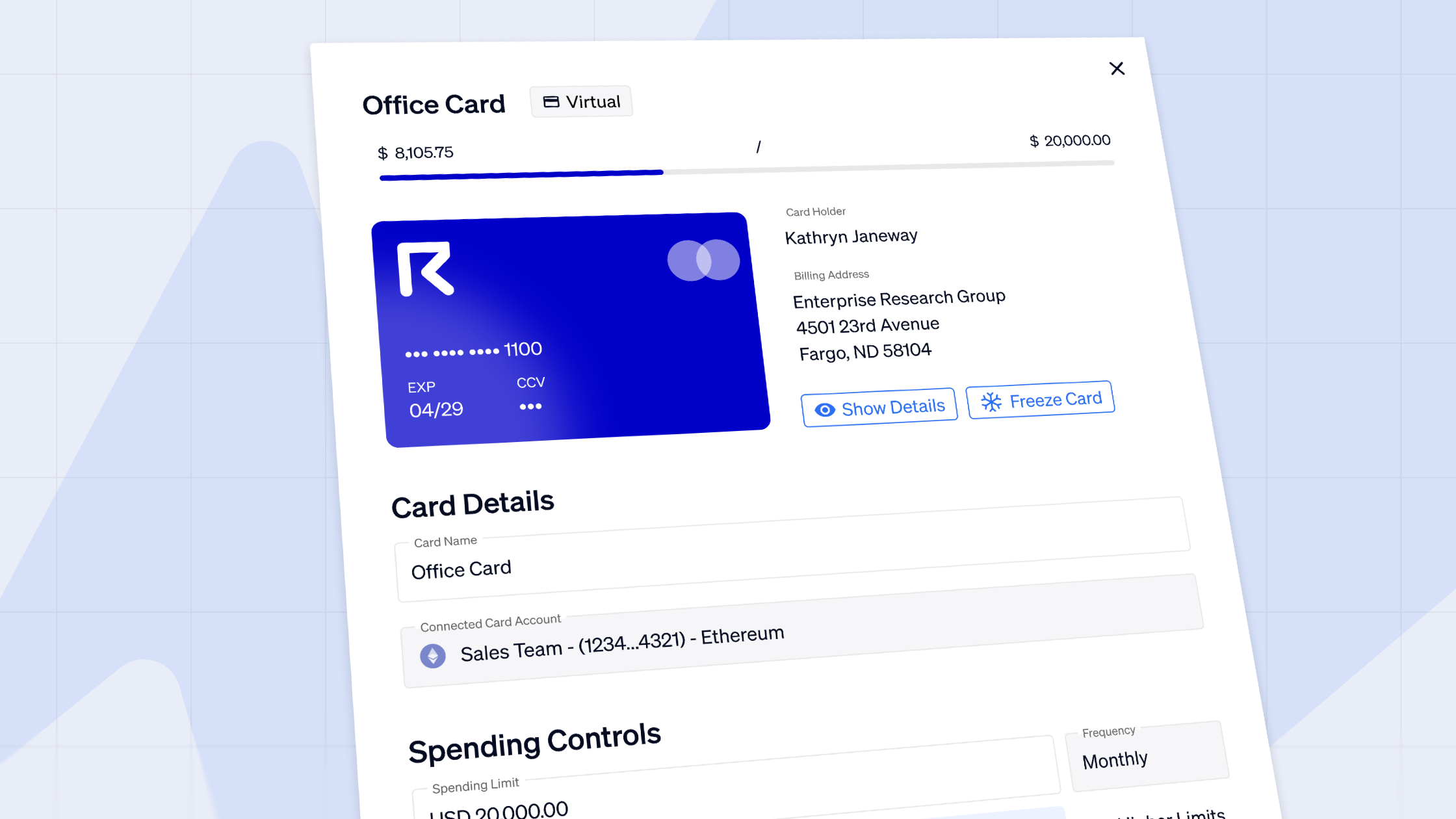

For instance, in Request Finance’s enterprise crypto payments app, users can easily pay, or get paid with the EURe stablecoin issued by Monerium, and directly cash out to any Single Euro Payments Area (SEPA) bank account in the Eurozone.

This is perhaps one of the simplest ways to move value from a bank account to a crypto wallet, and vice versa.

Pros

- Stable prices: ideal as a medium of exchange, and unit of account - two of the three defining features of money. Some of the most popular stablecoins such as USDC, BUSD, USDT and even some non-USD stablecoins like XSGD are issued by centralized entities in exchange for fiat currencies.

- Widely accepted and integrated into various crypto wallets: Allows for seamless transactions between bank accounts and crypto wallets. This makes it convenient for businesses to move value from a bank account to a crypto wallet and vice versa.

Cons

- Dependent on the trustworthiness and solvency of the stablecoin issuer: The ability of stablecoin issuers to meet redemptions is dependent on the reserves held by these entities. The composition and value of these reserves can vary, and there is a level of trust required in the issuer's ability to honor their debt obligations. For example, as of June 2022, approximately 75.6% of Circle's reserves consisted of 3-month U.S. Treasury Bills, while 24.4% was held in cash at regulated financial institutions. During the same period, U.S. Treasury Bills accounted for 58% of Tether's reserves.

- Limited availability to specific fiat currencies: May pose challenges for businesses operating in different regions or using non-mainstream currencies.

Ready to Supercharge Your Crypto Accounting?

Stop wasting time, manually creating journal entries. Automate your accounting now, and enjoy error-free reporting

Learn how to scale your company's crypto & fiat financial operations

Your financial complexities are our specialties. Schedule your free consultation today and discover how Request Finance can transform your financial operations

Simplify crypto and fiat financial operations today

Rely on a secure, hassle-free process to manage your crypto invoices, expenses, payroll & accounting.

2. Decentralized stablecoins

Unlike centralized stablecoins, decentralized stablecoins mint synthetic stablecoins when users deposit other crypto assets into a smart contract, rather than wiring fiat into a bank account of a deposit-taking institution.

These smart contracts aim to programmatically maintain a fixed exchange rate to a reference fiat currency, mimicking the decision-making processes and operations used by central banks or currency boards for their exchange rate policies.

For example, Curve, the second largest decentralized exchange on Ethereum, has released a whitepaper detailing an example of one such implementation of a price stabilization mechanism.

It’s technically not possible to directly deposit fiat currencies from bank accounts into smart contracts. Decentralized stablecoins exist in a middle ground between centralized stablecoins and centralized exchanges (CEXes). It’s still possible to off-ramp certain decentralized stablecoins in a roundabout manner that appears almost instantaneous.

Pros

- Global accessibility, not limited to USD stablecoins: Offers a range of non-USD stablecoins to conduct transactions in specific local currencies. For instance, Jarvis Network is a synthetic stablecoin protocol that operates on an over-collateralized basis and focuses on issuing non-USD stablecoins while creating liquid markets for them. Jarvis Network offers a range of non-USD stablecoins, including major currencies like jGBP, jCNY, and jEUR, as well as smaller and less represented currencies such as jSEK, jPHP, and jNZD.

- Beneficial for businesses operating in diverse markets: Non-USD stablecoins can enable Web3 companies to have deeper penetration into specific local markets. Through its partnership with Mt Pelerin Group, an authorized financial intermediary in Switzerland, Jarvis Network allows users to off-ramp decentralized stablecoins from any wallet on both Layer 1 and Layer 2 blockchain networks. It offers stablecoin off-ramps in 14 fiat currencies directly from bank accounts in 172 countries.

Cons

- Reliance on algorithmic mechanisms for stability and exchange rate: There’s a risk that a decentralized stablecoin will have a price meltdown.

3. Centralized exchanges

Centralized exchanges (CEXes) offer versatile on-ramps and off-ramps by accepting fiat bank deposits via bank wires or credit cards. Unlike stablecoins, CEXes facilitate the exchange of various cryptocurrencies and stablecoins for fiat currencies in many different currencies.

Pros

- Versatility in accepting various fiat currencies: Centralized exchanges typically accept fiat bank deposits via bank wires or credit cards, in many currencies, in exchange for most cryptocurrencies and stablecoins.

- Convenience of a single platform to on ramp and off ramp: This flexibility can be advantageous for businesses that require access to a wide range of cryptocurrencies and want the convenience of a single platform for their on-ramping and off-ramping needs.

Cons

- High fees, especially for credit/debit card transactions: Credit and debit cards are a popular way for retail users to purchase cryptocurrency via an exchange, but they come with high fees of up to 10% per transaction. Card payments are also on-ramps, but not off-ramps as it is usually impossible to “withdraw” money onto a credit or debit card.

- Risk of being de-banked: Many banks and credit card issuers still consider such transactions suspicious, locking or even closing accounts after learning the nature of the transactions. For exchanges, the credit cards of certain countries — including Russia and Ukraine — are automatically rejected.

Counterparty risks can often be higher: As a deposit-taking institution, it’s hard to assess whether a CEX has the liquidity and solvency to honor their debt obligations.

4. On-ramp vs Off-ramp: service providers

The number of options for direct payouts between crypto wallets and bank accounts is growing rapidly. Several players in this space offer these services, including non-bank financial institutions (NBFIs) such as online brokerages like Robinhood, fintech payment processors like Stripe, and neobanks like Revolut, which have recently started offering crypto services. These on ramp and off ramp providers effectively act as their own exchanges and market makers.

Among these providers are over-the-counter (OTC) desks, often operated by centralized exchanges (CEXes). OTC desks are particularly useful for conducting large transactions, typically involving millions of dollars, in a more cost-effective manner than spot purchases on exchanges.

Pros

- Efficient transfers of value: OTC desks are valuable due to their ability to conduct large trades without moving the market against them. This effect is known as “slippage” and occurs when large-scale buying causes prices to immediately rise before the targeted amount of cryptocurrency has been purchased, while selling causes it to fall before it’s all sold.

- Ideal for cases when large amounts have to be off-ramped: Cost efficient for scenarios such as converting a portion of the fiat capital raised in a venture funding round into stablecoins for global payroll purposes, or converting a portion of an organization's crypto treasury to fulfill bill payments that require a significant upfront cash downpayment, such as to landlords.

Cons

- Potential fees and limitations: Fees can vary depending on the provider and the nature of the transaction. Some providers may impose a flat fee per transaction, while others may charge a percentage-based fee calculated on the transaction amount.

Best Practices for On/Off Ramping

Navigating the on/off ramping process in the crypto industry poses challenges for businesses, particularly due to the nature of corporate banking and the associated risks.

Regardless of which off-ramp methods, or specific service providers you use to convert your fiat to crypto, or vice versa, these are the best practices to consider:

Map out your on/off ramp needs by payment corridors

Remember that on and off ramps ultimately mean having to deal with geographically-bound banking networks. Like the previous generation of web2 fintech payment processors, they are simply relying on a tech-enabled system to scale the ancient practice of Hawala banking to create the illusion of fast, global payouts.

To save yourself the time and frustration of being drip-fed limitations by various on/off ramp providers, you can map out your on/off ramp needs by payment corridors.

Go through your company’s database of employees, freelancers, contractors, and service providers. Map out the various country pairs, and the fiat payments volumes that flow between them. Armed with that knowledge, you will know which regions to prioritize on/off ramps for. This way, you can have more productive discovery calls with on/off ramp providers.

Avoid using on/off ramps to hold your treasury

On/off ramp wallets - especially third-party custodial ones, should never be abused as treasury wallets, to minimize your exposure to counterparty risk from custodians.

Too often, crypto companies are lulled into complacency, and end up misusing CEX wallets to hold significant amounts of their treasury.

If you had decided to move 500,000 USDC from your self-custodial treasury wallet to an FTX wallet now, and leave it there until the end of the month, you would have quickly found yourself out of a job. This is exactly what numerous startups, and even venture funds did for their employees - including FTX’s.

Implement a monitoring regime to screen for de-peg and liquidity risks

Whichever stablecoins you choose to use to on ramp vs off ramp, it is recommended that you set notifications and alerts for social media activity and price action to regularly screen for de-peg risks.

Apart from screening for warning signs for stablecoin de-peg risks on your own personal accounts, consider recruiting the help of your marketing team. They likely already have tools which monitor social media regularly as part of their workflows.

If your organization relies heavily on centralized stablecoin issuers to manage your organization’s on-ramps and off-ramps, you can regularly review the attestation or audit reports provided by these issuers as part of their disclosure regimes. Balance sheet issues could cause fatal bank runs. This also applies to screening for liquidity risks when using other centralized entities like CEXes for on and off ramps.

On the other hand, synthetic stablecoins are also subject to similar risks of their own, largely related to the design of their price stabilization mechanisms. You should review the design of these mechanisms closely, before deciding to rely on them as on-ramp and off-ramp channels. .

Regular screening can enable CFOs to react in a timely manner to protect their crypto treasury from such risks. There are numerous examples of how vigilant monitoring of fear, uncertainty and doubt, (FUD) on social media platforms has allowed individuals and companies to save hundreds of millions of dollars from exposure to collapsing stablecoins and centralized off-ramps.

There is safety in diversity

Ideally, you can use different on/off-ramp channels for different purposes. For instance, you can consider using a CEX to off-ramp crypto for payroll, and a centralized stablecoin issuer to off-ramp when paying SG&A expenses in fiat.

A simple rule of thumb is this - use at least two, uncorrelated, extensively-researched tools for each core activity area in your crypto finance stack: (i) crypto wallets, (ii) banking services providers, and (iii) on/off ramps.

You can focus on using multiple tools to de-risk these three core areas. They are the vital organs of your organization. Tooling failures here will immediately impact your balance sheet and liquidity.

By following these practices, your company can optimize your on/off ramping strategies and safeguard their financial well-being in the dynamic crypto landscape.

Crypto finance tips straight to your inbox

We'll email you once a week with quality resources to help you manage crypto and fiat operations

Trending articles

Get up to date with the most read publications of the month.

Our latest articles

News, guides, tips and more content to help you handle your crypto finances.

Master your crypto spend management now

Take control of your crypto spend management while relying on our safe and secure process.